SSS, PhilHealth & Pag-IBIG: The Complete Guide for Filipino Freelancers & Remote Workers (2026)

How to register, pay, and maximize SSS, PhilHealth, and Pag-IBIG as a Filipino freelancer. 2026 contribution tables, benefits, and pro strategies.

You're earning $800 a month from your remote job — maybe even more. But if you got hospitalized tomorrow, could you cover the bill? If you needed an emergency loan, could you get one approved in 24 hours? And when you eventually want to buy a house, will you qualify for a loan with a 5.75% interest rate?

For most Filipino freelancers and remote workers, the answer is no — because nobody told them that SSS, PhilHealth, and Pag-IBIG aren't just for corporate employees. These three government programs are your personal safety net: health insurance, retirement pension, emergency loans, and housing loans, all available to freelancers who contribute.

The catch? No employer is handling this for you. It's 100% your responsibility. And if you've been putting it off, every month you skip is a month you can never get back.

This guide walks you through everything: how to register, exactly what you'll pay, what you get in return, and the smart strategies that most guides don't cover.

Why you can't skip this (even if you're earning in USD)

Let's get one thing straight: these aren't taxes. SSS, PhilHealth, and Pag-IBIG contributions are more like forced savings and insurance that you can actually use. Here's what you're building with every monthly payment:

- Retirement pension — Monthly income for life starting at age 60

- Maternity benefits — Up to PHP 70,000+ for 105 days of paid leave

- Salary and emergency loans — Up to PHP 70,000 from SSS (based on your contribution level)

- Health coverage — Hospitalization costs covered through PhilHealth case rates (annual day limits removed effective April 2025)

- Housing loans — Up to PHP 6 million at 5.75% interest through Pag-IBIG, way below any bank rate

- Tax-free investment — Pag-IBIG MP2 earned a record 7.10% dividend in 2024, compared to ~0.25% from bank savings

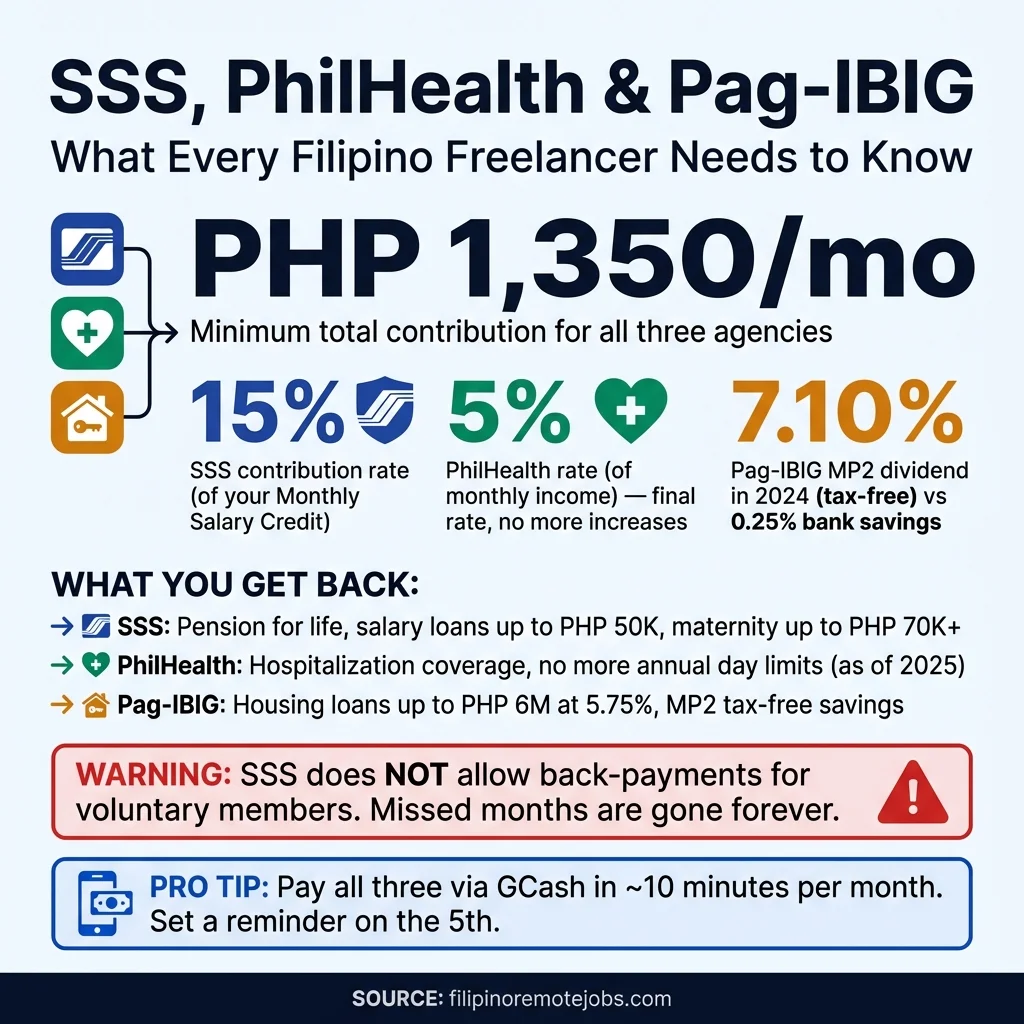

Now here's the part that hurts: SSS does not allow back-payments for voluntary members. If you skip a month, that gap is permanent. You can't pay a lump sum later to make up for years of inactivity. Every missed month pushes your retirement pension further away and reduces your loan eligibility.

One freelancer on Quora learned this the hard way: "I haven't paid a single cent to SSS. Can I pay some lump sum in the future to make up for all the years I've been inactive?" The answer was a flat no.

Start now, even if it's at the minimum. Future you will thank you.

Step 1: Register (or switch your status)

If you've ever been employed in the Philippines, you probably already have SSS, PhilHealth, and Pag-IBIG numbers. But here's what most people don't realize: your membership status doesn't automatically change when you leave your company. You need to manually switch to "voluntary" or "self-employed" to start contributing on your own.

Already a member? Switch your status

SSS: Log in to My.SSS, go to the E-Services menu, and submit a Member Data Change Request. Alternatively, fill out Form E-4 at any SSS branch. Change your member type to "Voluntary" or "Self-Employed."

PhilHealth: Submit an updated PhilHealth Member Registration Form (PMRF) online through the PhilHealth Member Portal or at any PhilHealth office. Update your membership category to "Direct Contributor — Self-Earning Individual."

Pag-IBIG: Log in to Virtual Pag-IBIG and update your Member's Data Form (MDF), or submit a Member's Change of Information Form (MCIF) at any branch.

Never been a member? Register from scratch

SSS: Create an account at my.sss.gov.ph and apply for an SS number online. You'll need a valid government ID. Activation link is sent to your email within minutes.

PhilHealth: Register online at the PhilHealth portal with a valid ID. Your PhilHealth Identification Number (PIN) will be emailed within about a week.

Pag-IBIG: Register entirely online through Virtual Pag-IBIG. Your Membership ID (MID) number is generated almost immediately. No need to visit a branch.

Pro tip: If you prefer in-person, you can do all three in one trip. SSS, PhilHealth, and Pag-IBIG offices are often located together in SM or Robinsons malls. One afternoon, and you're done.

Step 2: Know what you'll pay (2025-2026 contribution tables)

Here's the part everyone worries about. The good news: it's less expensive than you think, especially at the lower brackets. And both SSS and PhilHealth rates have reached their final scheduled caps under current law (RA 11199 and RA 11223 respectively) — no further increases are scheduled.

SSS contributions (15% of your declared Monthly Salary Credit)

As of January 2025, the SSS contribution rate is 15% of your Monthly Salary Credit (MSC). As a voluntary member, you pay the full amount yourself.

You choose your MSC based on your actual monthly income. Higher MSC means higher contributions, but also bigger pension, bigger loans, and bigger maternity benefits later.

| Monthly Salary Credit | Monthly Contribution |

|---|---|

| PHP 5,000 (minimum) | PHP 750 |

| PHP 10,000 | PHP 1,500 |

| PHP 15,000 | PHP 2,250 |

| PHP 20,000 | PHP 3,000 |

| PHP 25,000 | PHP 3,750 |

| PHP 35,000 (maximum) | PHP 5,250 |

Bonus: For MSC above PHP 20,000, excess contributions go into your MySSS Pension Booster (Mandatory Provident Fund), which is basically an extra retirement savings account on top of your regular pension.

PhilHealth contributions (5% of monthly income)

PhilHealth uses a flat 5% rate on your declared monthly income. This is the maximum rate under the Universal Health Care Act (RA 11223) — no further increases are scheduled under current law.

- Minimum: PHP 500/month (income floor of PHP 10,000)

- Maximum: PHP 5,000/month (income ceiling of PHP 100,000)

If you earn PHP 20,000/month, you pay PHP 1,000. Simple math.

Pag-IBIG contributions

Pag-IBIG is the cheapest of the three. As a self-employed member, you pay both the employee and employer shares:

- Income over PHP 1,500: 2% + 2% = 4% of income

- Maximum: PHP 400/month (capped at fund salary of PHP 10,000)

- Minimum: PHP 100/month for voluntary members

Total monthly cost at different income levels

Here's what it all looks like together, translated to the dollar incomes many remote workers earn:

| Your Monthly Income | SSS | PhilHealth | Pag-IBIG | Total |

|---|---|---|---|---|

| ~$90 (PHP 5,000 — minimum) | PHP 750 | PHP 500 | PHP 100 | PHP 1,350 |

| ~$435 (PHP 25,000) | PHP 3,750 | PHP 1,250 | PHP 400 | PHP 5,400 |

| ~$610 (PHP 35,000) | PHP 5,250 | PHP 1,750 | PHP 400 | PHP 7,400 |

| ~$870 (PHP 50,000) | PHP 5,250 | PHP 2,500 | PHP 400 | PHP 8,150 |

At the minimum bracket, PHP 1,350 per month gets you access to pension, health insurance, loans, and housing — for less than the cost of a Netflix and Spotify subscription combined.

Step 3: Pay your contributions (the easy way)

You don't need to wait in long government office lines anymore. You can pay all three from your phone in about 10 minutes.

Online payment (GCash, Maya, bank apps)

SSS via GCash (most popular method):

- Log in to My.SSS and generate a 14-digit Payment Reference Number (PRN) — this is required before paying

- Open GCash → Bills → Government → SSS Contribution

- Enter your PRN, amount, and payor type

- Confirm payment (a small convenience fee applies — check the GCash app for current charges)

PhilHealth: GCash → Bills → Government → PhilHealth. Enter your PhilHealth number and amount. Also available through Maya, BDO, Metrobank, and other bank apps.

Pag-IBIG: Pay directly through the Virtual Pag-IBIG portal using linked bank accounts, credit cards, GCash, or Maya.

Over-the-counter options

Prefer cash? You can pay at SM Bills Payment counters, Bayad Center, 7-Eleven, and any SSS/PhilHealth/Pag-IBIG branch.

Payment schedule

PhilHealth offers monthly, quarterly, semi-annual, or annual payment options. SSS and Pag-IBIG are typically monthly.

Pro tip: Pick one day each month — say the 5th — and batch all three payments together. Set a phone reminder. It takes about 10 minutes total through GCash. Miss a month for SSS and you can never fill that gap.

What you actually get back (benefits breakdown)

This is the section that makes your contributions worth it. You're not just paying into a void — here's exactly what each program gives you back.

SSS benefits

Sickness benefit: 90% of your average daily salary credit, for up to 120 days per year. You need at least 3 monthly contributions within the 12 months before getting sick.

Maternity benefit: 100% of your average daily salary credit for 105 days (normal delivery) or 120 days (solo parents). At a higher MSC, this can mean PHP 70,000 or more — paid directly by SSS to your bank or e-wallet. You need at least 3 contributions in the prior 12 months.

Retirement pension: Monthly income for life starting at age 60 (optional) or 65 (mandatory). You need 120 total contributions — that's 10 years. The longer you contribute and the higher your MSC, the bigger your pension. Without 120 contributions, you only get a one-time lump sum, which is significantly less.

Salary loan: Up to two months' worth of your Monthly Salary Credit — that's up to PHP 70,000 at the maximum MSC of PHP 35,000. Interest is 8% per annum (diminishing balance), with 24-month repayment. You need 36 monthly contributions for a one-month loan, or 72 for a two-month loan. Voluntary members can apply online through My.SSS.

Calamity loan: Up to PHP 20,000 at 7% annual interest, payable in 24 monthly installments. Available when SSS activates the program for a specific natural disaster affecting your area.

Funeral benefit: PHP 20,000 to PHP 60,000 for beneficiaries (with 36+ contributions).

PhilHealth benefits

Hospitalization: Case rate packages cover room and board, medicines, labs, and professional fees. Per PhilHealth Circular 2025-0007 (signed March 20, 2025, effective April 4, 2025), the 45-day annual confinement limit has been permanently removed.

Increased coverage: In January 2025, PhilHealth increased approximately 9,000 benefit packages by 50%. For example, pneumonia coverage went from PHP 19,500 to PHP 29,500.

Z-Benefits: Coverage for catastrophic illnesses including cancer, kidney transplants, and more — with coverage running into hundreds of thousands of pesos.

Konsulta Package: Free outpatient consultations, health screenings, basic lab tests, and preventive dental services at accredited clinics.

Important caveat: PhilHealth operates on case rates. It covers a set amount per condition, not your total bill. For full protection, consider supplementing with a private HMO.

Pag-IBIG benefits

Housing loan: Up to PHP 6 million at 5.75% annual interest (1-year repricing) or 6.25% (3-year repricing). Pag-IBIG occasionally offers promotional rates for first-time homebuyers — for example, a 4.5% rate for loans up to PHP 1.8 million was offered in late 2025 under the Expanded 4PH Program (limited slots, with income eligibility requirements). Check with Pag-IBIG for current promotions. One Upwork freelancer shared how a Pag-IBIG assessor "delightfully approved" their PHP 550,000 housing loan using their Certificate of Earnings.

Multi-purpose loan: Up to 90% of your total regular savings (increased from 80% in May 2025). Now only requires 12 monthly contributions, reduced from the previous 24.

Calamity loan: Up to 90% of savings at 5.95% annual interest.

MP2 Savings: This is Pag-IBIG's best-kept secret. It's a voluntary savings program that earned a record 7.10% dividend in 2024 — and dividends are completely tax-free. Compare that to a typical bank savings account at 0.25%. One investor put PHP 30,000 into MP2 and earned roughly PHP 12,000 in interest over 5 years. The same amount in a bank would have earned PHP 377.

Pro moves: Maximize your benefits

Now that you know the basics, here's how to get the most out of these programs.

Contribute at a higher MSC (SSS)

Your pension, loan amounts, and maternity benefits are all calculated based on your Monthly Salary Credit. Contributing at the minimum (PHP 5,000 MSC) means minimum benefits. If you're earning $800–$1,500/month remotely, consider declaring a higher MSC in the PHP 15,000–25,000 range. The extra PHP 1,000–2,000 per month now could mean tens of thousands more in benefits when you need them.

Open an MP2 account (Pag-IBIG)

If you have any extra savings, MP2 is one of the best low-risk investments available in the Philippines. Here's why:

- 7.10% dividend rate in 2024 (record high) — dividends vary yearly based on fund performance

- Tax-free — no taxes on your earnings

- Government-guaranteed principal — your savings are protected (per Pag-IBIG's official MP2 FAQ), though dividends are not guaranteed

- Minimum PHP 500 per deposit

- 5-year maturity — your money is locked in, which helps if you're a spender

Open one through Virtual Pag-IBIG in about 5 minutes.

A note on tax deductions

A common misconception: SSS, PhilHealth, and Pag-IBIG contributions are not deductible from your BIR taxes when you're contributing as a voluntary or self-employed member. They're still worth paying for the benefits alone — just don't count on them reducing your tax bill. Check out our freelancer tax guide for what you can actually deduct.

Common mistakes to avoid

These are the most frequent mistakes we see in freelancer communities, and every one of them is avoidable.

Not switching your status after leaving a company. Your SSS, PhilHealth, and Pag-IBIG memberships don't automatically change when you resign. If you don't update to "voluntary" or "self-employed," your contributions simply stop — and nobody tells you.

Planning to "catch up later." SSS does not allow retroactive payments for voluntary members. Missed months are permanent gaps. If you need 120 contributions for a retirement pension, every skipped month pushes that goal further out.

Contributing at the minimum when you can afford more. Your pension amount, loan limits, and maternity benefits are all tied to your contribution level. Minimum in, minimum out.

Not tracking your payments. Log in to My.SSS, PhilHealth portal, and Virtual Pag-IBIG at least quarterly to verify your contributions are being posted correctly. Payment errors happen.

Assuming PhilHealth covers everything. PhilHealth uses case rates — a fixed amount per condition. Your actual hospital bill can be significantly higher. Consider adding private HMO coverage, especially if you don't have employer-provided health benefits.

Waiting until you need benefits to start contributing. Maternity and sickness benefits require at least 3 months of contributions in the prior 12 months. SSS salary loans need 36 total contributions. If you start paying only when you're already pregnant or sick, you won't qualify.

Your action plan

Setting up your government contributions takes about 30 minutes. Maintaining them takes about 10 minutes per month. Here's your checklist:

- This week: Register or switch your status for all three agencies (SSS, PhilHealth, Pag-IBIG)

- This month: Make your first contribution through GCash or your preferred payment method

- Set a monthly reminder: Pick a day (the 5th works well) and batch all three payments

- Consider your MSC level: If you can afford more than the minimum, contribute more — your future self benefits

- Explore MP2: Open an account and start with PHP 500 if you want a tax-free investment

You're already building a career as a remote worker. Now build the safety net to protect it. When you're ready to find your next remote opportunity, browse current job listings on Filipino Remote Jobs — and this time, you'll have the financial foundation to match your ambition.

Already handling your government contributions? Make sure your taxes are sorted too — read our Freelancer Tax Guide for the Philippines for the complete BIR walkthrough. And if you're still figuring out the best way to receive payments from international clients, check out our Wise vs PayPal vs Payoneer comparison.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or tax advice. Contribution rates, benefit amounts, loan terms, and program eligibility are subject to change. Always verify current rates and requirements directly with SSS, PhilHealth, and Pag-IBIG or consult a licensed professional before making financial decisions. Information in this guide is based on publicly available sources as of February 2026.

Get Remote Jobs in Your Inbox

Join Filipino professionals getting curated remote job opportunities delivered every week. No spam, unsubscribe anytime.

Share this article

About Filipino Remote Jobs Team

The Filipino Remote Jobs Team is dedicated to helping Filipino professionals find legitimate remote work opportunities with international companies. We provide career advice, job search tips, and insights to help you land your dream remote job.

Related Articles

Freelancer Tax Guide Philippines: BIR Registration & Filing for Remote Workers (2026)

Complete guide to BIR registration and tax filing for Filipino freelancers and remote workers. Learn the 8% tax option, quarterly deadlines, and how to stay compliant while working for international clients.

AI Tools for Filipino Remote Workers: How to Work Faster, Earn More, and Stand Out (2025)

Discover free AI tools that Filipino VAs, freelancers, and remote workers are using to boost productivity and land higher-paying clients. Practical tips for the Philippine context.

Negotiate Your Remote Salary: Scripts & Benchmarks for Filipinos (2026)

Copy-paste salary negotiation scripts for Filipino remote workers. Includes 2026 salary benchmarks by role, tips for countering geo-based pay, and real examples.